VUTHISA has been on the forefront of improving emissions from pyrolysis equipment especially of the type used in developing countries. Herewith our concept document to make sense of the charcoal industry in South Africa. Our study includes the types of systems being used and approximate cost of such systems and market potential of charcoal. Part of our conclusion is to produce Emission Reduction kilns that is also portable and this is discussed at the end.

To get full access to this report either purchase a GOLDEN TICKET or support us on PATREON.

BACKGROUND

There are two basic methods of making charcoal; direct and indirect. The direct method requires a fairly simple process, low capital investment and little technical know-how. The direct method uses heat from the incomplete combustion of the organic matter which then becomes charcoal. The rate of combustion is controlled by regulating the amount of oxygen allowed into the burn and is stopped by excluding oxygen before the charcoal itself begins to burn. In South Africa charcoal is widely produced, using the direct method, in small metal or masonry kilns. The indirect method uses an external source of heat to cook the organic matter contained in a closed but vented airless chamber (retort). This is a more advanced process requiring substantial know-how and high capital investment. Some of the leading South African charcoal manufacturers use the indirect method to produce charcoal. The bulk of charcoal in South Africa is produced by the direct method in rural areas close to the sources of commercial timber supplies. Production units generally consist of 4 steel kilns, grouped into small clusters, to form economic production units. Economy of scale does not seem to play a big role in the primary production phase and therefore production units vary from small clusters, producing between 8 and 120 tons of charcoal per month to sophisticated retort plants such as those operated by E&C Charcoal in KwaZulu-Natal. Economic benefits are, however, realised if downstream activities such as packaging, screening and marketing are centralised and done on a larger scale. Locally produced charcoal is essentially distributed to three key markets which include: The local household market where charcoal is used for barbeques. This is a highly specialised and competitive market. Products are sold in packaged form and distributed through retail outlets to the household market. The local industrial market where charcoal is used primarily as a reduction agent in non-ferrous metal processing. By far the largest user is Silicon Smelters. Exports mainly of packaged and branded products for the overseas barbecue market. This market became especially buoyant when the Rand devaluated sharply against the Euro, BP, USD and Sterling. With the recent strengthening of the Rand this market has become more competitive and is especially threatened by large-scale cheap supplies from Indonesia and South American countries notably Brazil.

THE SUPPLY AND DEMAND FOR CHARCOAL

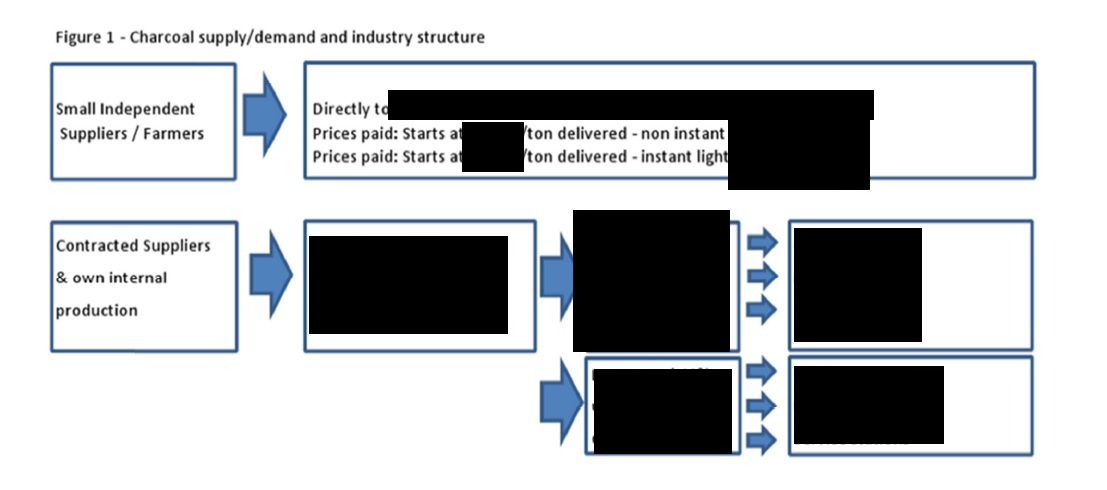

A schematic presentation of the current supply and demand situation in South Africa is presented in Figure 1 below.

The household market, which uses briquettes and charcoal lumps as a relatively clean fuel for barbeques, dominates the demand. The industrial market uses natural charcoal lumps as a reducing agent in non-ferrous melting processes. The South African market for household charcoal is supplied by many small informal operators and the larger industrial companies which supply branded products through established retail chains, petrol stations and smaller retailing groups, e.g. cafes, hardware stores, etc. This market is competitive but prices achieved are more than twice as high as that obtained for industrial charcoal. About 25% of total domestic production is exported as packaged branded products for the overseas barbecue market. Exports are sensitive to the value of the Rand and at current rates local exporters find it difficult to compete internationally. The production of charcoal is mainly concentrated in the Natal Midlands area and south-eastern parts of Mpumalanga, stretching from Ermelo down to Pietermaritzburg. A few small plants are operating in the Eastern Cape and in the Limpopo province; the latter supplying mainly in the requirements of Silicon Smelters. Silicon Smelters indicated that they need to import considerable amounts of charcoal from regions outside Limpopo as the availability of suitable raw materials (hardwoods) limits production in that province. Silicon Smelters is constantly looking for new sources of supply and indicated a keen willingness to assist any potential small-scale entrepreneurs in setting up charcoal production units. Charcoal lumps, in an unrefined form, are supplied by many small contracted or independent small-scale producers. In fact, about 80% of all primary charcoal is produced by independent small-scale operators. In the case of the industrial market the unrefined charcoal is normally packed into 50 kg bags, collected by the user which then refines the product for its own internal use. Some smaller industrial users are supplied directly by producers. The major charcoal producing companies purchase the bulk of their raw material from contracted suppliers. They produce some charcoal internally, mainly through the indirect method using sophisticated retorts. These companies add value to the charcoal raw material by screening the charcoal, compressing it into briquettes and by packaging, branding and distributing the product country wide through wholesalers and retailers. Most of the products handled by these charcoal suppliers are for the household market and are sold mainly in 5 kg bags. A new trend has emerged in the form of Instant Light whereby wax is sprinkled over charcoal and packaged into 1 or 1.5 kg brown paper bags, with 2 bags packed into a 2, 2.5 or 3 kg bag. Prices paid by trade stores are around R 23/bag even though the product weighs 50% less, so more profits are achieved with Instant Light.

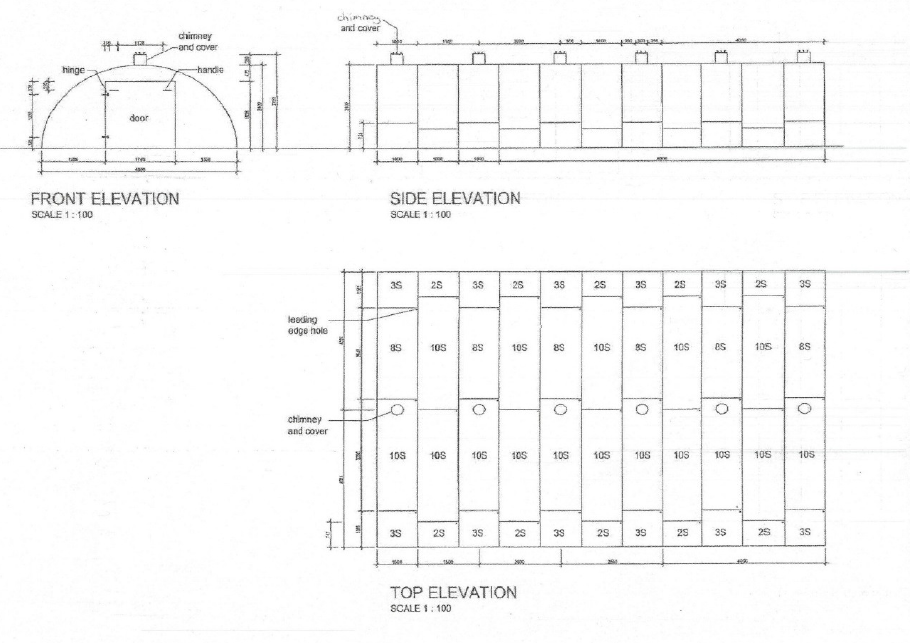

ARMCO kilns

Another popular charcoal production system is produced in kit form in Isando, Gauteng and is made from corrugated iron sheet metal by Armco Superlite (Pty) Ltd. Armco units come in 12 metres lengths and two or four kilns are grouped together and produce 2 to 3 tons of charcoal per kiln per burn. The most popular size is a 12 m kiln cut in half and bricked up on one side. Monthly turnover is conservatively estimated at R480 000 with a net income of R144 000. The total capital investment for a production unit (with a capacity of 120 tons/month) consisting of four 6 m kilns including flat packed transport to site, chain saws for harvesting and a small tractor-trailer combination could be R500 000 to R700 000. An operation this size will need a workforce of around 40 people.

Additional costs are mentioned in the last paragraph of Technical Parameters.

TECHNICAL PARAMETERS

Wattle and hard gums (E.nitens and E.dunni, E.Cleoziana) are the preferred raw material for charcoal production in South Africa. The characteristics of the preferred hardwoods are basically as follows:

1 m³ = 600 kg (semi dry wood). The conversion ratio of charcoal is 6:1, i.e. 6 kg of semi dry hardwood is required to produce 1kg of charcoal. Based on the above ratios 1 m³ of semi-dry hardwood yields 100 kg of primary charcoal. Primary charcoal consists of charcoal lumps, fines and ash. This primary product is further screened and processed to separate useable charcoal lumps from fines and ash. Suitable lumps are then packed in 50 kg bags and shipped to the industrial plants or packaged as branded products for the barbecue market. Charcoal briquettes are produced from fines which are compressed with a binding agent and maize starch to form a uniform fuel. The bulk of the household demand is for briquettes which account for an estimated 60% of the total domestic barbecue market. The production output and timber requirements for an efficiently run Converted Underground Fuel Storage production unit, consisting of four, 25,000 L kilns, are calculated as follows:

- Number of production cycles per kiln per annum =

36 - Intake of timber per kiln per cycle =

10 m3 or 8 t - Production output per kiln per cycle =

1.5 ton - Thus, annual charcoal output (

4kilns x36cycles/kiln x1.5tons/kiln/cycle) =216tons - Total income at average price of R

5000/ton = R1 080 000p.a. - Estimated net income/profit for owner operator = R

324 000p.a. - Timber intake requirement (

4kilns x36cycles x10m³/cycle/kiln)1,440m3 =1100tons =1,440m³/annum - Plantation area required to sustain operation =

192ha - Clear felling area required for 1 year’s operation =

8ha

Note: Above projections are for burning conservatively once/week, and this can be increased to twice/week.

The production output and timber requirements for an efficiently run Armco production unit, consisting of four, 6 m kilns, are calculated as follows:

- Number of production cycles per kiln per annum =

150 - Intake of timber per kiln per cycle =

30m³ - Production output per kiln per cycle =

3ton - Thus, annual charcoal output (

4kilns x150cycles/kiln x3tons/kiln/cycle) =1 800tons - Total income at average price of R

4000/ton = R7 200 000 p.a. - Estimated net income/profit for owner operator = R

2 160 000p.a. - Timber intake requirement (

4kilns x150cycles x30m³/cycle/kiln)18,000m3 =13800tons - Plantation area required to sustain operation =

2 400ha - Clear felling area required for 1 year’s operation =

200ha

Charcoal producers cannot afford to pay much for standing timber as the production process and the final prices do not allow for expensive input materials. Most raw material is obtained free of charge from clearing wattle jungle and wattle infested areas; through the Work for Water Programme and as a service to land owners for clearing their land. It is therefore unlikely that normal commercial plantations could be a sustainable raw material resource for charcoal production. The use of commercial plantations for this purpose could only be considered if no other markets are available, if jungle or neglected areas need to be cleared or where large-scale wattle infestation occurs that needs to be cleared. Costing models calculate that a maximum of R 50 /ton can be paid to growers. If however a partnership can be formed with contractors to leave “black timber” during their felling operations to extract pulp timber there would be no need to pay for harvesting or the grower. The participation of contractors is in the first levels of the value chain, i.e. up to the production of primary charcoal. About 85% of all employment opportunities are also in the first levels, including mainly harvesting and transporting of timber and burning of charcoal. The packaging, screening and briquetting (not included in this report) are costly processes and add an estimated R1000/ton to the value of primary unprocessed charcoal. It is also recommended to source a mobile office, on-site army style tents for accommodation, storage tents or containers, ablution facilities, JOJO tanks for drinking water and dousing of flames. For the production of Instant Light Charcoal special wax is required which VUTHISA has the recipe for. VUTHISA can make available costing models.

EMPLOYMENT

It is estimated that the charcoal industry employs in excess of 6 000 people. Of this about 75% are employed in the small-scale contracting sector which is mostly located in deep rural areas. The employment estimate is based on full time employment equivalents. A substantial amount of harvesting and timber collection is, however, sub-contracted on a piece work basis to family members and other available workers within the communities. These people work on an ad hoc basis and are being paid based on the volume of timber delivered. On the basis of this the industry probably provides livelihoods for many more people than the 6 000 stated above which represent equivalent full time employees.

In addition to job creation, the industry provides ample opportunity for entrepreneurial development as most of the small contracting units are operator owned. The sector therefore provides empowerment opportunities in developing small business units owned by local rural people. VUTHISA TECHNOLOGIES have in the past trained people in the art of making charcoal under the Fibre Processing & Manufacturing (FP&M) SETA and this should be investigated.

MARKET CONSIDERATIONS

The domestic market for barbecue charcoal is very competitive with four major suppliers competing in the sector. With increasing consumer expenditure, due to lower interest rates, the market is reported to be booming at present and considerable growth is forecast for the medium term. The export market is becoming increasingly competitive especially with the strengthening of the Rand against the currencies of major markets in which the local product is marketed. Stiff competition at cut-throat prices is also now being experienced from South American and Indonesian suppliers. There are rumours however that these supplies will not be sustainable as raw materials are obtained from indigenous forests, utilising harvesting and production processes that could not be certified. Locally, wattle raw material is becoming scarcer especially in KwaZulu-Natal where there is increased competition for this resource from large chipping enterprises that export hardwood chips to pulp mills in Japan. Some manufacturers are now importing raw materials from Namibia and Zimbabwe. The Eastern Cape is considered as one area where considerable raw material, especially from wattle infested plantations, is available. Previous attempts to establish a significant charcoal sector along the lines of subcontracting have however failed. Large charcoal users such as Silicon Smelters and producers of charcoal for the barbecue markets are interested in obtaining new sources of primary charcoal. Silicon Smelters, which are contemplating expansion of their production facilities, are especially concerned about the lack of charcoal production and raw materials in the Limpopo province. They are extremely keen to cooperate with contractors and would in their words “take every bit of charcoal that could be supplied” from willing suppliers. They are prepared to fund and supply contractors with the necessary kilns and support equipment as well as with medium to long-term contracts for supply of charcoal. They would provide the necessary training and assistance to ensure economic viability and sustainability of production. They are also extremely keen to consider joint ventures with DEA or any new future owners of the plantations to source hardwoods for charcoal production in the Limpopo region. In their attempt to secure future charcoal supplies they have moved into certain Eastern Cape areas. Their efforts to establish a sub-contracting industry in that region came to very little. Mondi tried to enter the market with their Black Gold project but that failed due to various reasons but mainly due to unscrupulous partners being allowed to run riot by supplying inadequate sources/species of timber and being allowed to sell the charcoal to whomever without oversight and proper allocation of profits to Trusts. The aim of this project was to provide job opportunities to unemployed staff and to use available wattle jungle and other hardwoods on a productive basis, but jungle areas were quickly eradicated resulting in timber having to be transported at great cost as repositioning of kiln was time-consuming and expensive. In summary it would seem that there is a good market for industrial charcoal and that primary users in this market are very keen to form joint ventures and to assist prospective small-scale operators in becoming part of the supply chain. The local market for value-added barbecue charcoal is very competitive but growing at a rapid rate.

IMPLICATIONS AND LESSONS

The configuration of a small-scale production unit makes it ideal for operation by a local community, a rural cooperative or as a small business unit. In many cases production units are run by families. It would therefore seem that all the ingredients are available for successful SME development and the involvement of poor rural people and communities in the sustainable production of charcoal. These key success factors for small-scale charcoal production include:

i) Cheap raw material supply

ii) Available capital from large market players to become involve withsmall-scale producers in a joint venture basis

iii) Available captive markets, both in terms of large industrial users andproducers of value-added and branded packaged products.

iv) The local supply of kilns at reasonable prices. The current kilnproducer indicated its willingness to provide the necessary training andtechnical back up to small-scale operators entering this market

All the above seem to be in place, supporting the viability of small-scale charcoal production. In previous sections it has been shown that small-scale charcoal production:

Is a labour intensive industry; employing women on a large scale.Creates jobs and household income in rural and poor areas where other income generating opportunities are scarce.Works well (many examples confirm this) and is an ideal rural entrepreneurial activity and lastlyalready interests big players who are willing to continue supporting SMEs.

RECOMMENDED APPROACH

Approaches to make charcoal production work for poor communities

especially in Limpopo, Mpumalanga, Kwazulu-Natal and the Eastern Cape

include:

i) Promote the use of timber raw materials from the WfW programme andparts of Category B and C plantations for value added charcoalproduction.

ii) Involve other large plantation owners to make available plantationwaste for charcoal production – as per the Mondi Blackgold example.

iii) Promote the concept of charcoal production amongst poor communitiesthrough DEA’s clusters by means of extension services.

iv) Arrange workshops with key players, .e.g. E&C Charcoal, SiliconSmelters, etc, and communities to develop co-operative charcoalproducing joint ventures.

v) Over the medium to longer term small charcoal producers could formjoint ventures or co-operatives amongst themselves to add furthervalue to lump charcoal – thus producing high value packaged productfor the household market. Even exports could be considered.

ALTERNATIVE MOBILE EMISSION REDUCTION & BIOCHAR APPROACH

VUTHISA offers an alternative approach for charcoal operations in mountainous and inaccessible areas in close proximity to large masses of biomass. A study by Airshed on our Emission Reduction kilns states the following conclusion:

|

Our emission data were compared to standard emissions produced by charcoal making kilns in developing countries. [Pennise et al (2001). Emissions of greenhouse gases and other airborne pollutants from charcoal making in Kenya and Brazil. Journal of Geophysical Research | Vol. 106 | No. D20 | Pages 24, 143-24,155 | October 27, 2001]

Apart from the emissions reduction component, the char product produced also has high adsorption qualities and is therefore an excellent BIOCHAR production system. See report below in which VTK1 and VTP1 are VUTHISA kilns being compared to activated carbon produced by CCC1:

A further development was the incorporation of a refractory mesh screen covered in fibre plaster to increase the longevity of the kiln sheet metal and which will also result in an increase in thermal efficiency (upwards of 60% improvement). Our latest model is a rectangular model consisting of modular, square, 3CR12 panels to simplify construction and flat-packing for transport over mountainous terrain.

It is also now possible to link any number of kilns in series to further improve overall fuel efficiency and pre-drying of feedstock. Usually off-gases and excess heat are vented indiscriminately into the atmosphere which is inexcusable.

The use of rocket stoves to pre-dry feedstock is also a viable and cheaper solution to the above system:

I hope this blog post was informative. Please click on the “Contact Us” page and get in touch with further questions or if you wish to invest in any if the above systems. Also consider purchasing a VUTHISA GOLDEN TICKET or visit our PATREON to unlock this full report receive one on one correspondence and guidance in designing a system that best suits your needs: